A Few Thoughts on Banks

The 2011 thesis on big American banks, that they were under-earning, cheap on tangible book, and destined to normalize, had largely played out by 2018, yet the case for holding wasn't finished. Overcapitalized and returning nearly all their earnings through buybacks and dividends, with rising rates and flat costs at their backs, the banks could still deliver double-digit returns, provided the credit cycle didn't intervene.

PDF Read the original — 2 figures, fully formatted ↗You guys thought I was kidding when, years ago, I said you’re going to have a golden age of banking…well you have a golden age of banking. With all the regulatory issues, some of which are disappearing, satisfaction scores are up everywhere, in almost every bank in almost every business. If you look at the financial results of JPMorgan Chase alone, they’re extraordinary and consistent year after year after year after year after year. And it’s not just us, okay? Even in ’08, we had a 7% return on tangible equity— that’s pretty good…So I think these banks have annuity businesses: custody, cash management, asset and wealth management—even part of trading is consistent: hedging, FX around the world, capital expenses, and investments. Obviously, there’s an episodic part, but people forget about the consistent parts. So to me, yes, these are pretty powerful franchises and profitability is being restored to the ones that didn’t have it.

Jamie Dimon on June 1, 2018 (lightly edited for brevity)

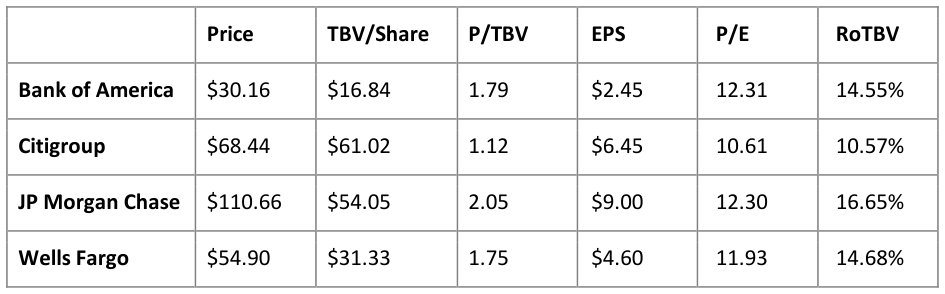

We have been invested in various large U.S. banks since 2011—it has been a long and bumpy (but nonetheless very rewarding) ride. The original investment case was simple: the banks were temporarily under-earning their tangible equity, their earnings would normalize over time, and upon reaching this normalized return on tangible equity, their price to tangible book value (P/TBV) would also return to historic multiples of 1.5 to 2. This thesis has largely been proved out: for example, in 2011, Bank of America had a share price of ~$6 and a tangible book value per share of ~$13 (P/TBV of 0.46), but after Q1 of 2018, Bank of America has a share price of ~$30 and a tangible book value of ~$17 (P/TBV of 1.76).

Most value investors, us included, expected that this normalization of both the returns on and multiples of tangible book value would be the conclusion of our bank investment. However, after reaching this point, we believe there is potentially more to the story : the large U.S. banks are currently overcapitalized and should be able to return 100% or more of their earnings to shareholders over the coming few years; their earnings and returns on tangible equity have improved considerably due to tax changes and increases in interest rates; they have good exposure to further expected increases in interest rates; and they will likely continue to grow while holding expenses steady.

Current State of Banks

Prior to the first quarter of 2018, it was somewhat difficult to accurately estimate the bank’s future earnings because of the recent tax reform; however, with the results of the quarter now in hand, their earnings have become a little easier to model, as shown in the table below.

U.S. Large Bank Estimated 2018 Earnings

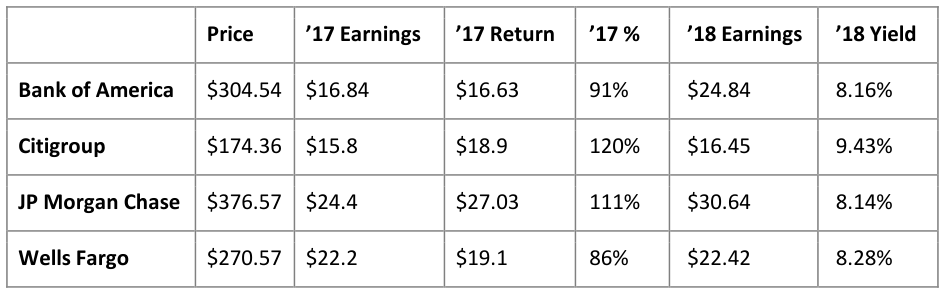

Importantly, capital returns for the large banks are currently high and expected to increase. For example, Citigroup has indicated that it believes it can return $60 billion dollars over the next three years; JP Morgan has indicated its payout ratio should be around 100% over the “medium term”; Wells Fargo has indicated that its payout ratio will be elevated for the next few years; and Bank of America has indicated its capital levels are far in excess (by $15-$20 billion) of what they need to be. Thus, all of the banks are overcapitalized by varying degrees, and they plan to return large amounts of capital for the foreseeable future . In fact, they can continue to return these high levels of capital until each bank either: 1) reduces its overcapitalization by returning more than 100% of earnings and/or 2) increases its balance sheet sufficiently to require retention of the current excess capital. Moreover, both Citigroup and Bank of America still have deferred tax assets to use, even after the write-down from tax reform.

In summary, shareholders can expect virtually all of the estimated 2018 earnings to be returned via dividends and buybacks. The following table shows the percentage of 2017 capital return relative to 2017 earnings and the estimated earnings yield for 2018, using current market capitalizations.

Thus, assuming 100% return of estimated 2018 earnings, the buybacks and dividends alone provide a high single-digit annual return for investors. Additionally, as mentioned above, Citigroup has guided to $20 billion or more returns for 2018, which would be a yield of 11.5% from current market levels.

Possible Returns

Besides the capital return, there are other positive investment factors to consider. For example, most of the banks are projecting modest top-line growth in the coming years as well as multiple increases in interest rates. At the same time, costs are expected to be controlled, resulting in positive operating leverage. For example, Citigroup expects the overhead ratio to decrease from a current 57% to 53% over the next few years. Over the same time period, Bank of America has indicated that it expects its $53 billion of costs to remain steady while revenues increase. These increase in revenues and steady or reducing overhead are expected to occur while returning 100%+ of earnings, which mathematically means that earnings should organically increase at decent rates and that returns on tangible equity must correspondingly increase due to both an increasing numerator and a decreasing denominator.

On top of these mathematical expectations, several banks have explicitly indicated that they are expecting higher returns on tangible equity. For example, Citigroup has targeted 12% for 2019, 13% for 2020, and 15% or more in the future. Wells Fargo has indicated the possibility of 17% by 2020, and Bank of America has similarly stated that mid-high teens are possible under the assumption of moderate revenue growth while holding costs steady.

Using simple models that combine capital return with increases in earnings and returns on tangible equity, shareholders may easily get 10%+ annual returns from any of the large banks . In fact, Bank of America and Wells Fargo could yield mid-teens annual returns while Citigroup could reach high-teens (or even higher) annual returns if they are able to achieve the targets they have discussed.

Potential Issues

There are obviously scenarios where these returns do not manifest—banks are notoriously cyclical (particularly Citigroup), so their multiples typically decline during any negative macro events, and their earnings would assuredly drop in a recession. Additionally, banks have a history of looking cheap before a crisis happens: for example, in 2008, earnings multiples were not high and several high-profile value investors made the case that Wachovia and other financials were cheap.

However, while cyclical, banks are much better capitalized than before and are passing stress tests that model scenarios more severe than the 2008 crisis. In fact, in the 2015 JP Morgan annual letter, Dimon stated: “ JPMorgan Chase alone has enough loss absorbing resources to bear all the losses, assumed by CCAR, of the 31 largest banks in the United States .” Thus, while a recession could be painful to shareholders, the banks should have more than enough capital to continue to operate.

A turn in the credit cycle could be more concerning. For many years after the crisis, credit was very tight; however, credit has been loosening for quite some time, and there are clear concerns in sub-prime auto as well as other areas. The current low reserving for bad loans is not sustainable and would modestly reduce the banks’ earnings in a more normal environment and strongly reduce them during a credit crisis. However, it is difficult to estimate the magnitude of these effects, and it is also possible that their overall impact may still allow for good returns from present prices. Indeed, Jamie Dimon provided comments on through-the-cycle profitability of banks on June 1, 2018 (again edited for brevity):

This is through the cycle, so we know when we’re over-earning: we’re over-earning right now in middle market credit—we’ve had no middle market credit losses for years. We told you we were over-earning in credit cards…so we try to manage the risk through the cycle. We’re pretty comfortable that—if you look at our results, we’ve been earnings 13 to 15% on tangible equity through the cycle, even with some under earning, some over earning, some excess expense and stuff like that, so we’re pretty comfortable that we’ll be able to earn in that range. I don’t know about the 17%, but we have really good returns in tangible equity.

Remember, if you have 15% returns on tangible equity, that means you will double every five years. That is an unbelievable thing if we can accomplish that for our shareholders, just that one thing. That’s better than most hedge funds, better than most private equity, better than most investments, and we’ve been doing it. Now, if you can reinvest at that kind of rate, and we think we’ll have opportunities to do that for the foreseeable future, that’s huge value for shareholders. We know we have some episodic businesses, but we don’t overreact to episodic businesses, and we try to invest through the cycle. There’s no magic to 12 months, there’s no magic to a cycle, so we kind of look through all that and we want you, the client, to be really happy with our products and services and our pricing. If we under earn or over earn, so be it, but we’re pretty comfortable we can do that of the foreseeable future.

If the market begins to believe that the banks can withstand recessions and maintain through-the-cycle profitability at the 15% level, it is possible that bank earning’s multiples could increase from their current levels to the 13-15 range, which would yield even more upside for current investors. Time will tell.